by

by Introduction: Choosing the Right Life Insurance

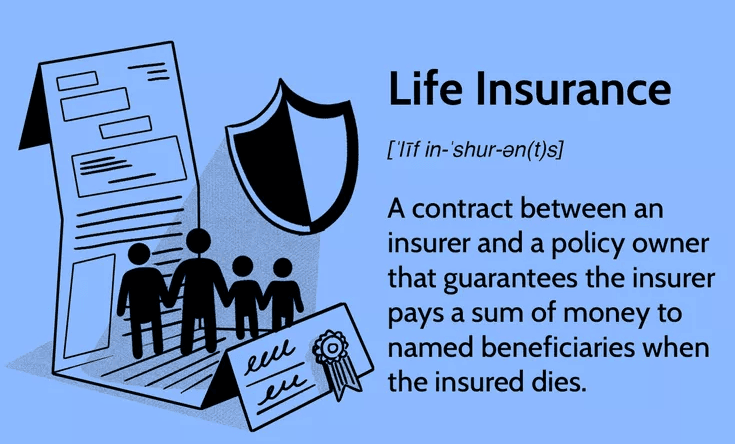

Life insurance isn’t the most exciting thing to think about, but it’s one of the smartest financial decisions you can make for your loved ones. When shopping around, you’ll probably face the big question: “Should I get Term Life Insurance or Whole Life Insurance?” Each type has its own perks, drawbacks, and ideal use cases. Choosing the wrong one could cost you thousands—or leave you under-protected. This guide will break down Term Life vs. Whole Life Insurance, so you can confidently pick the best option for your needs. Let’s dive in!

What Is Term Life Insurance?

Term life insurance provides coverage for a specific period of time—usually 10, 20, or 30 years. If you pass away during the term, your beneficiaries receive a tax-free death benefit. If you outlive the term, the coverage expires (unless you renew or convert it). . Think of it as “renting” life insurance coverage for a set amount of time.

Key Features of Term Life Insurance:

- Fixed term length (10, 20, 30 years, etc.)

- Level premiums (fixed payments) during the term

- No cash value accumulation

- Typically much cheaper than whole life

- Option to renew or convert to permanent insurance (sometimes)

What Is Whole Life Insurance?

Whole life insurance is a type of permanent life insurance. It lasts for your entire life as long as you keep paying the premiums.In addition to the death benefit, it includes a cash value component that grows over time (often at a guaranteed minimum rate).Think of it as buying life insurance coverage plus a savings account.

Key Features of Whole Life Insurance:

- Coverage lasts your entire life

- Guaranteed death benefit

- Cash value grows tax-deferred

- Can borrow against the cash value

- Premiums are much higher than term life

Term Life vs. Whole Life Insurance: Head-to-Head Comparison

Let’s compare them side by side.

| Feature | Term Life Insurance | Whole Life Insurance |

|---|---|---|

| Duration | Fixed term (10-30 years) | Lifetime coverage |

| Premiums | Lower | Higher |

| Cash Value | No | Yes |

| Flexibility | High (can convert or let expire) | Lower (long-term commitment) |

| Ideal For | Temporary needs (mortgage, income replacement) | Long-term wealth building and estate planning |

| Cost Over Time | Increases if renewed after term | Remains consistent |

Pros and Cons of Term Life Insurance

✅ Pros:

- Affordable premiums (especially when young)

- Simple and straightforward to understand

- Flexible: Buy coverage only when you need it

- Ideal for short- to medium-term needs (mortgage, raising kids)

❌ Cons:

- No cash value (pure insurance only)

- Coverage expires after term

- Renewal premiums can be very expensive as you age

- If you outlive the term, you get nothing back

Pros and Cons of Whole Life Insurance

✅ Pros:

- Lifetime coverage guarantees your family a payout

- Cash value can be used during your lifetime (loans, withdrawals)

- Predictable premiums and returns

- Helps with estate planning and leaving a legacy

❌ Cons:

- Expensive premiums (5–10x more than term life)

- Can be complicated (fees, loan rules, surrender charges)

- Not the best option if you only need temporary coverage

- Returns on cash value may be lower than other investments

How Much Does Each Type Cost?

Here’s a general idea (though actual rates vary based on age, health, and policy size):

| Age | Term Life (20-Year, $500,000) | Whole Life ($500,000) |

|---|---|---|

| 30 | ~$20–$30/month | ~$300–$500/month |

| 40 | ~$30–$50/month | ~$400–$600/month |

| 50 | ~$70–$100/month | ~$600–$900/month |

💵 Term life is dramatically cheaper, making it more attractive for younger families.

When Should You Choose Term Life Insurance?

Term life is often the best fit if:You need coverage for a set period (raising kids, paying off a mortgage) , You want affordable premiums to fit your budget , You’re young and healthy and want maximum coverage for low cost , You plan to self-insure later by building enough savings. New parents, young couples, and homeowners often favor term policies.

When Should You Choose Whole Life Insurance?

Whole life may make sense if: You want lifetime coverage guaranteed , You like the idea of building cash value over time ,You have complex financial needs (estate planning, business succession) , You have extra income to afford higher premiums .High earners and people looking for long-term wealth strategies often opt for whole life.

What About a Combination Approach?

Some people combine both types for the best of both worlds.

Example Strategy:

- Buy a large term policy for major short-term needs (like income protection)

- Layer in a small whole life policy for lifelong benefits and cash value

This way, you protect your family now and build permanent security for the future without overspending.

Term Life vs. Whole Life: Key Questions to Ask Yourself

Before choosing, ask:

- How long do I need coverage?

- What’s my current financial situation?

- Do I want life insurance strictly for protection—or also as an investment?

- Can I comfortably afford higher premiums over decades?

- Do I need estate planning tools?

🧠 Pro Tip: If budget is tight, prioritize term life first. You can always add whole life later when finances improve.

Final Verdict: Which Life Insurance Is Better for You?

| Choose Term Life if… | Choose Whole Life if… |

|---|---|

| You need affordable, temporary coverage | You want lifetime protection and cash value |

| You have dependents or a mortgage to cover | You’re planning for long-term wealth transfer |

| You expect to self-insure later through savings | You can afford high premiums comfortably |

There’s no one-size-fits-all answer.

The “best” life insurance depends entirely on your personal goals, stage of life, and financial situation.

When in doubt, speak with a licensed insurance advisor to craft a policy that matches your needs perfectly.