by

by Introduction: Business Insurance Isn’t Just for Big Corporations

When you’re running a small Business Insurance, you wear a lot of hats: manager, marketer, customer service rep, accountant—and more. With so much going on, business insurance might not be at the top of your to-do list. But it should be.One lawsuit, one fire, or one unexpected disaster could wipe out your hard-earned progress in an instant.

Business insurance protects your dream and keeps you afloat when life throws the unexpected your way.In this guide, we’ll explore why every small business should have insurance, what types you might need, and how to choose the best coverage.

What Is Business Insurance?

Business insurance is a broad term that covers several types of protection designed to safeguard your company’s financial well-being.Depending on the policy, it can cover: Property damage, Lawsuits, Employee injuries, Data breaches, Business interruptions And much more. In short: business insurance protects you against risks that could otherwise destroy your company.

1. Protect Your Business Assets

Imagine waking up to find your storefront flooded or your office ransacked. Could you afford to replace everything out of pocket?Property insurance, a key part of business coverage, protects physical assets like: Buildings, Equipment, Furniture, Inventory, Signage. Without it, even a minor disaster could cause major financial loss. Whether you operate from a home office, a retail space, or a warehouse, asset protection is a must-have.

2. Shield Yourself from Lawsuits

In today’s litigious world, even the smallest businesses face the threat of lawsuits. Common legal threats include: Customer injuries (slips and falls) , Product liability claims ,Contract disputes, Professional mistakes or negligence. General liability insurance helps cover the costs of legal defense, settlements, and judgments.

Without it, a single lawsuit could bankrupt your business.Even if you win the case, legal fees alone can cripple a small business financially.

3. Ensure Business Continuity After Disasters

Natural disasters, fires, thefts, or even power outages can disrupt your operations for days, weeks, or even months. Business interruption insurance helps cover: Lost income , Rent or mortgage payments , Employee salaries , Relocation costs (if necessary). This type of coverage ensures that you can pay your bills and stay afloat while recovering from unforeseen disruptions. It’s your financial lifeline when things go sideways.

4. Protect Your Employees (and Meet Legal Requirements)

If you have employees, you’re often legally required to carry: Workers’ compensation insurance (covers workplace injuries) , Unemployment insurance ,Disability insurance (in some states). Even beyond legal obligations, caring for your team with proper insurance builds loyalty and shows you value their well-being. A healthy, secure team means a healthier, more stable business.

5. Enhance Your Credibility

Having the right insurance can make your business more attractive to customers, clients, partners, and investors. Clients feel reassured when they know you’re properly insured. In fact, some larger companies or government contracts may require proof of insurance before doing business with you. Being insured signals that your business is trustworthy, stable, and professional.

6. Cover Cyber Risks

Small businesses are increasingly targets for cyberattacks—and the costs can be devastating. Cyber liability insurance can cover: Data breach response ,Legal costs from customer lawsuits , Fines and penalties ,Reputation repair. Even a simple phishing attack could lead to tens of thousands of dollars in damages. If you store customer data (even email addresses), you should seriously consider cyber coverage.

7. Peace of Mind for You, the Owner

Running a small business is stressful enough.

The last thing you need is to lie awake at night worrying about what would happen if something goes wrong. With the right insurance, you can: Focus on growth instead of fear , Take calculated risks ,Plan confidently for the future. Business insurance isn’t just protection—it’s peace of mind.

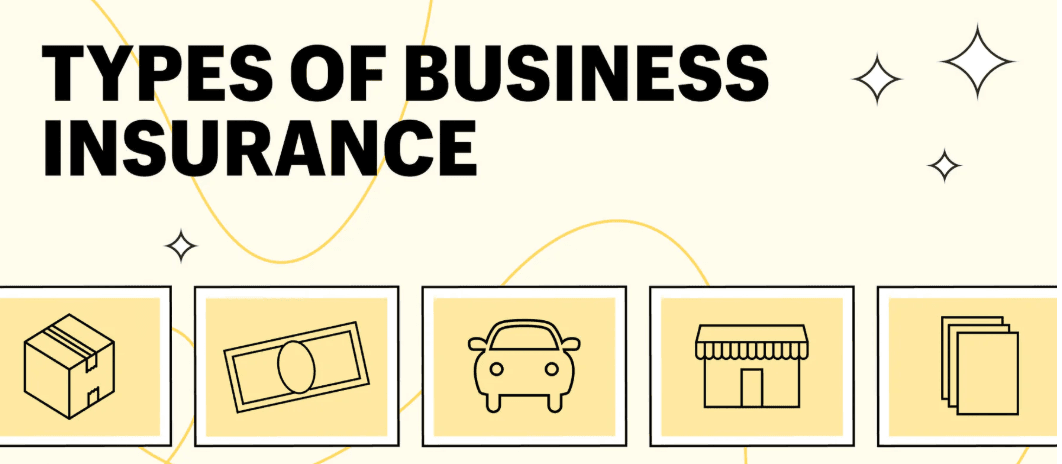

Types of Business Insurance Every Small Business Should Consider

Depending on your industry, size, and risks, here are the key types of coverage you might need:

| Insurance Type | What It Covers |

|---|---|

| General Liability | Bodily injury, property damage, legal defense |

| Commercial Property | Physical assets like buildings and equipment |

| Business Interruption | Lost income and operating expenses after a disaster |

| Workers’ Compensation | Employee injuries or illnesses |

| Professional Liability | Errors, omissions, negligence claims |

| Cyber Liability | Data breaches, cyberattacks |

| Commercial Auto | Vehicles used for business purposes |

| Product Liability | Defects or damage caused by your products |

Real-World Examples: How Insurance Saved Small Businesses

🏠 A Boutique Clothing Store:

A small boutique suffered a fire that destroyed its inventory. Property insurance covered the rebuilding and replacement costs, allowing the store to reopen within months.

🍽️ A Catering Business:

An allergic reaction at an event led to a lawsuit. General liability insurance covered legal defense and medical costs, saving the business from bankruptcy.

💻 A Web Design Firm:

A hacker stole client data. Cyber insurance paid for legal fees, notification costs, and credit monitoring services for affected clients, preserving the firm’s reputation.

What Happens If You Don’t Have Business Insurance?

Without insurance, you’re gambling your entire livelihood. Risks of being uninsured include: Paying out of pocket for damages, lawsuits, or losses ,Losing business contracts that require insurance, Personal financial ruin (if your business debts fall back on you) ,Permanent closure due to an unexpected disaster .Skipping insurance is a huge gamble—one most small businesses can’t afford.

How Much Does Small Business Insurance Cost?

The cost varies widely depending on: Industry ,Business size and revenue ,Number of employees , Location ,Coverage types and limits. On average, small businesses pay $500–$3,000 per year for general liability coverage. But one claim can cost tens of thousands—making insurance a smart investment.

How to Choose the Right Business Insurance

Here’s a simple plan:

- Assess your risks:

- What could go wrong?

- What would it cost to fix?

- Research policy types:

Understand what protections match your risks. - Get multiple quotes:

Compare prices and coverages. - Work with a broker:

A good insurance agent can help tailor a package for your specific needs. - Review and update regularly:

As your business grows, your insurance needs will too.

🛠️ Business insurance isn’t “set it and forget it”—it evolves with your company.

Final Thoughts: Protect Your Business, Protect Your Future

Running a small business takes passion, courage, and a whole lot of hard work.

Don’t let all that effort go to waste because of one unexpected event.

Business insurance is not a luxury—it’s a necessity.

It protects your finances, your employees, your customers, and your dream.

It gives you the confidence to grow, expand, and weather any storm.

✅ Smart businesses are insured businesses. Don’t wait until it’s too late.